Navigating the Emotional and Financial Complexities of Lending to Loved Ones

A strange phenomena occurs when your success becomes public knowledge. Many friends and family come flocking whenever there is a business idea to explore, a cause to donate to, or a problem to be solved.

So, how do you decide when to loan and when not to? A good rule of thumb is to anticipate not receiving a return on your investment and only to loan money if it’s money you can “afford to lose."

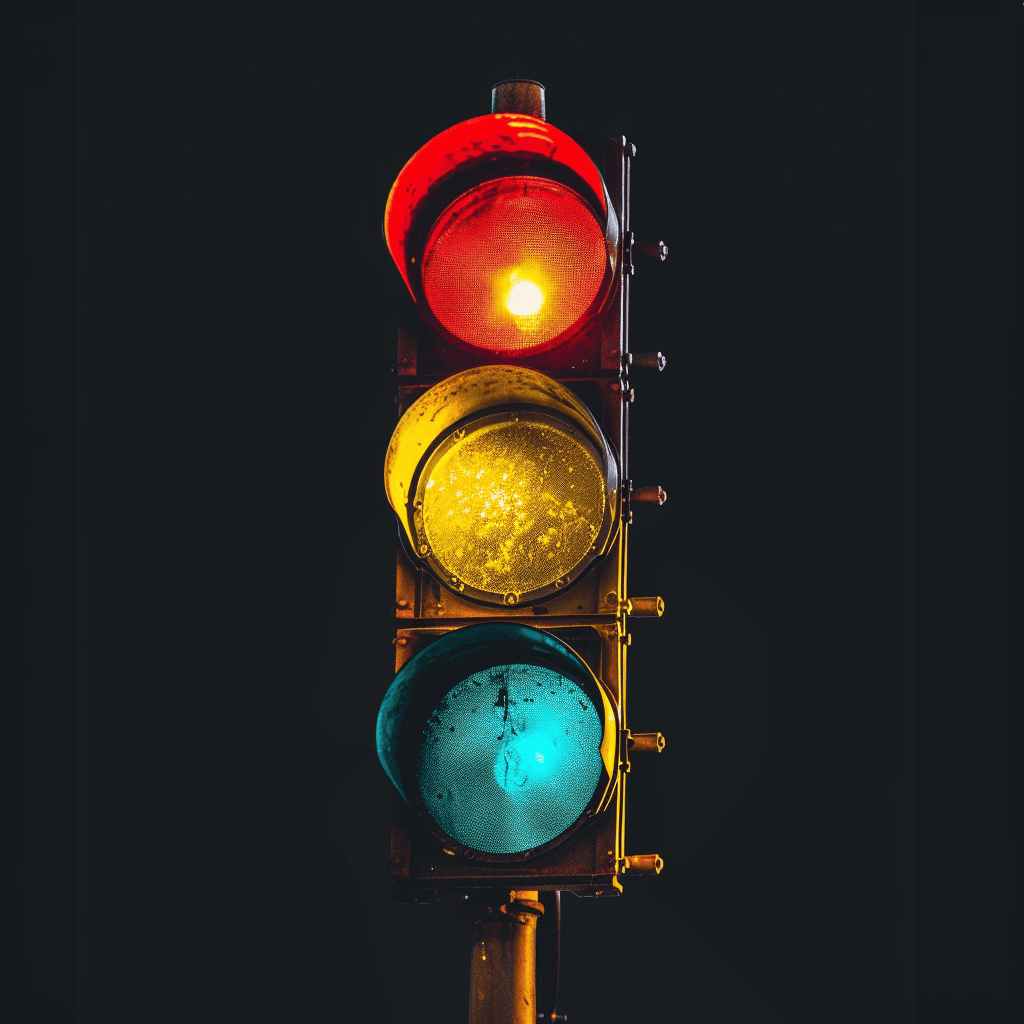

Here’s a “Red, Yellow, Green” formula for deciding what you can “afford to lose”:

Red: If they’re asking for a huge amount of money, you should act on the contracting guidelines (I outline some below). Make sure you evaluate the request thoroughly with your team of advisors and then think it through.

Yellow: The money they’re asking for is important to you, and you don’t want to lose it. But if you did, it wouldn’t be the end of the world.

Green: Hand it out and stop worrying about it. It won’t affect you, but it will benefit them.

Of course, you can always make a gift of the money. Remember to make a clear distinction between a gift and a loan. When you make it a gift, make it simple. Just give it to them and make it clear that you do not expect to be paid back.

When you do decide to make a loan to friends or family, ask yourself:

“Is this an asset problem or a behavior problem?”

You can’s solve a behavior problem with assets.

Ultimately, you can’t throw money (an asset) at a behavior problem and expect a good outcome. If you’ve given money before, or they have gone to others for support, and their behavior hasn’t changed, it is very likely that pointing more money at the problem won’t solve it.

Instead, the behavior needs to change before more money will be effective. A single mother who’s working to pay the bills but her car (asset) is broken down has an asset problem. To solve it, you need an asset (car or money). But if your kid keeps saying they’ll make better choices (behavior) but they need help financially (assets) to get back on track, that’s a behavior problem, and throwing assets won’t change your their behavior.

Get it in writing.

Make a contract and both of you sign it. The contract should include the date of the loan, the amount of the loan, the minimum payments and the period (monthly, yearly, etc.), the interest rate (if applicable), the due date for payment in full, and the consequences of defaulting on the loan. You might think, “How can I subject my sister or my old college friend to something as impersonal as a contract?” A contract can avoid miscommunication and limit hard feelings later on. You can always change the contract if needed, but its very existence makes it more likely that the terms of the loan will be met and the relationship preserved.

Prepare to lose your money emotionally.

Ask yourself if the money or the relationship is the most important. Such a loss could permanently damage your relationship with the borrower. You should decide upfront how you will respond in your heart and mind if he or she defaults. By committing to not lend money to friends and family you don’t want to lose and expect to not get paid back, you can avoid straining your closest relationships. You can preserve dynamics around the Thanksgiving table and avoid making things awkward if they default.

For people who are really in need but you’d rather not become a lender, there are other ways to help. You can review business plans and budgets and give the benefit of your knowledge and expertise. You can help them identify lenders or investors who can fill the need. Or, if they can work for you in some way, they can earn the money. I, of course, would love everyone to be able to give as much as they feel they are able. But, like most things in life, clear boundaries and ground rules for giving are important in creating a broader impact.

Regardless, the decision to loan or not to loan is a deeply personal one, with a lot of emotional implications. Take the time to determine what strategy works best for you and your family and then hold to that boundary you set with your loved ones. This can help you protect your relationships and your assets.